You are running a high-frequency algorithmic market-making or arbitrage script under heavy volatility, and your console suddenly flashes a catastrophic warning: APIError(code=-2010): New order rejected.

Unlike parameter validation warnings or timestamp drifts, Error -2010 means your API syntax is flawless, but the exchange’s core execution engine has actively refused to put your order on the books. In the 2026 multi-asset professional trading landscape, this error can lead to unhedged directional exposure and immediate drawdowns. Here is the institutional blueprint to isolate and bypass the -2010 deadlock.

The Root Structural Causes of Error -2010

Through advanced multi-asset trading and deep technical market analysis in 2026, we have mapped the specific structural triggers for this error into three operational categories:

- The Margin Account Liquidity Lock: If your bot is trading perpetual futures or using isolated margin mode, -2010 triggers when your current maintenance margin ratio is too close to the liquidation threshold. The system blocks new risk-increasing exposure while allowing only reduce-only execution.

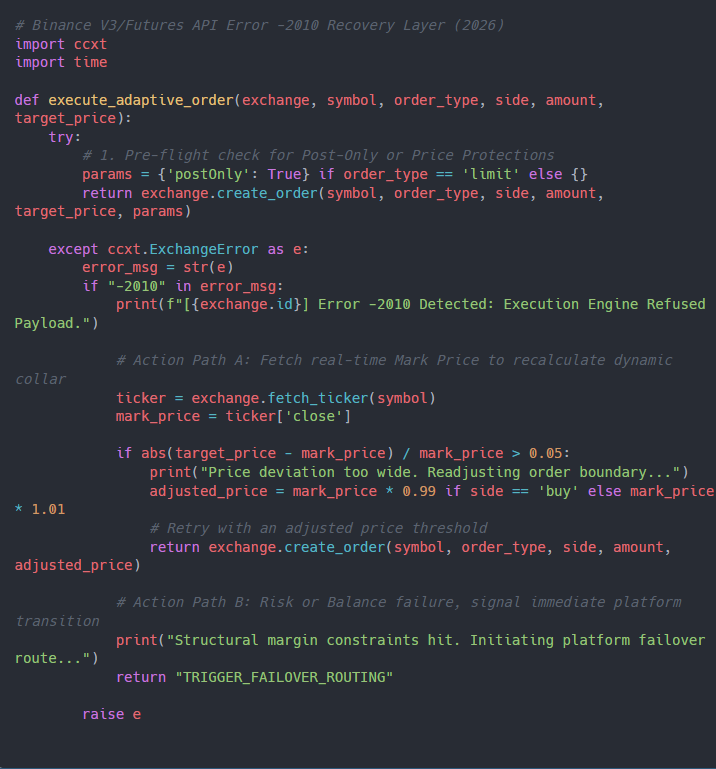

- The “Price Protection” Filter Trigger: In 2026, to prevent flash-crashes caused by rogue market-order scripts, matching engines enforce a strict percentage deviation cap against the current Mark Price. If your automated limit order is placed outside this dynamic collar, it is instantly rejected with a -2010 flag.

- The Post-Only Order Mismatch: If your high-frequency framework utilizes the

POST_ONLYexecution instruction to guarantee maker fee rebates, and the market moves fast enough that your order would immediately cross the order book as a taker, the matching gateway drops a -2010 error to protect your fee profile.

The Technical Fix: Pre-Flight Risk Check and Type Guarding

To prevent your script from freezing when the execution engine throws a -2010, you must deploy pre-flight risk checks and adaptive price collars. Use this clean production-grade Python wrapper to catch the exception, adjust boundaries, and deploy automated recovery paths.

Hardening System Resiliency: Multi-Venue Redundancy

When an exchange’s execution gateway continuously rejects risk allocation via -2010 under high-volatility conditions, professional algorithmic operations immediately route capital flow into secondary networks. Relying on a single infrastructure cluster is an obsolete operational model.

The Strategic Redundancy Matrix:

- The Primary Quant Alternative (Bitget): Renowned for its streamlined V2 infrastructure designed to handle overflow trading volumes without cascading rejection faults. Claim your access through the Bitget VIP Quant Portal ($80 Bonus).

- Advanced Portfolio Margining Hub (OKX): Offers decoupled multi-leg liquidation shielding and superior Web3 engine stability via the OKX Developer Portal.